When companies compare Fixed and Variable Rate (FAVR) reimbursement programs, one question comes up all the time:

“Why are one provider’s fixed and variable rates different from another’s?”

Program inputs shape how a FAVR reimbursement is calculated. Things like company-selected vehicle requirements, retention cycles, and Business Use Percentage (BUP) all influence the structure of the program and how final reimbursements are determined for drivers.

At the same time, FAVR calculations rely on real-world cost data that changes over time. Fuel prices, insurance rates, maintenance costs, and regional driving expenses can all fluctuate throughout the year. Providers may update this data at different intervals or use different methodologies behind the scenes, which can affect reimbursement accuracy over time.

That means small differences between FAVR rates are completely normal.

At first glance, choosing a FAVR provider based on their provided rates seems like a simple decision criteria. But it’s important to remember that FAVR is shaped by a lot more than the final reimbursement number.

The bigger question is whether the reimbursement methodology stays current, localized, and aligned with real-world driving costs over time.

Because vehicle costs are always changing. Insurance premiums move. Fuel prices fluctuate. Vehicle prices rise and fall. Maintenance costs vary by region and vehicle type.

A compliant and audit-proof reimbursement program should evolve alongside those changes.

What Actually Makes Up a FAVR Rate?

At its core, a FAVR reimbursement is built around one simple idea: reimbursing employees for the cost of owning and operating a vehicle for business use.

To do that, the program relies on a series of standard “vehicle assumptions.” These are the assumptions used to estimate what driving actually costs.

That includes things like:

- Vehicle type

- Insurance costs

- Fuel prices

- Retention periods

- Maintenance and repairs

- Registration and taxes

- Local driving costs

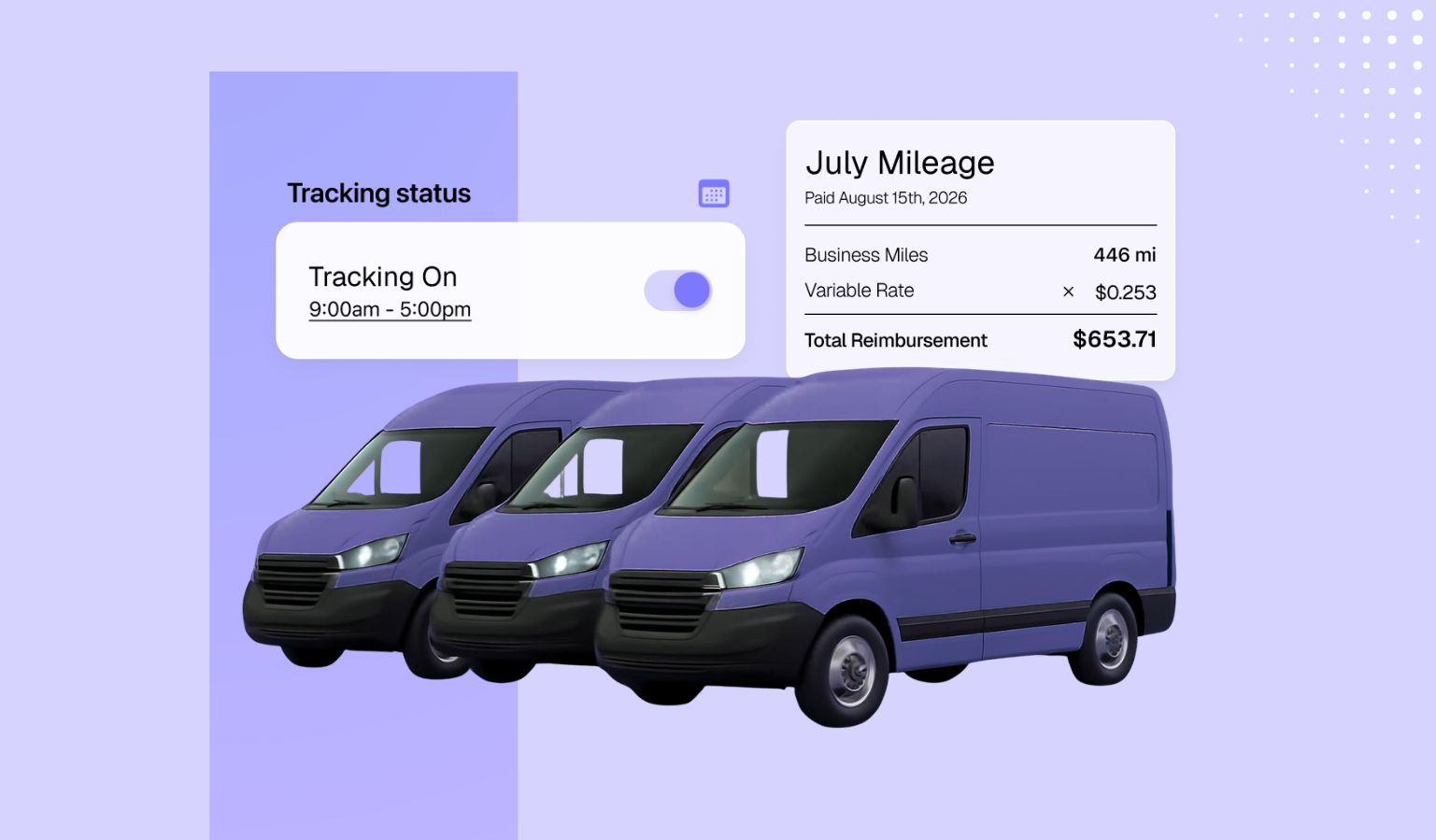

FAVR programs separate these required vehicle expenses into two categories:

- Fixed costs, which stay relatively stable month to month

- Variable costs, which change depending on miles driven

For example, insurance and depreciation are considered fixed costs. Fuel and maintenance are variable costs because they increase as mileage increases.

Different providers may build these assumptions differently.

One provider might update insurance data quarterly. Another may update it annually. One provider may model newer vehicles with current market pricing, while another might rely on older vehicle profiles or longer retention cycles.

Even small differences in methodology can produce different reimbursement outputs.

That is why two compliant FAVR programs may not generate identical rates.

The most important thing to consider, though? Whether the assumptions behind the program still reflect current driving costs and market conditions.

Why FAVR Rates Naturally Change Over Time

One of the biggest misconceptions about vehicle reimbursement programs is that reimbursement rates should stay stable forever.

But in reality, vehicle costs are always changing.

Insurance premiums increase or decrease depending on claim trends and local markets. Fuel prices fluctuate throughout the year. Vehicle prices shift with supply chains, interest rates, and manufacturing costs. Depreciation changes as resale markets change.

Even the cost of maintaining a vehicle varies over time.

Anyone who has paid for tires, repairs, or routine maintenance recently has seen that firsthand.

Regional costs also matter. Driving in downtown Chicago does not cost the same as driving in rural Texas. Insurance, fuel, taxes, traffic patterns, and repair costs can vary significantly by location.

That is why FAVR programs are designed to evolve with the market.

A reimbursement program should not stay frozen while the underlying costs of driving continue changing around it.

When reimbursement assumptions stay current, the program remains aligned with real-world business driving costs.

When assumptions stop evolving, reimbursement accuracy can slowly drift over time.

Where Things Can Start to Get Complicated

One real challenge with FAVR programs is making sure reimbursements stay accurate as vehicle costs change over time. Whether a reimbursement amount is too high or too low absolutely matters.

But behind that question is something even more important: whether the methodology underneath the reimbursement is still current, reasonable, and defensible. Because problems can start when reimbursement outputs continue increasing while the underlying vehicle assumptions remain outdated.

With some providers, that can happen in several ways:

- Older vehicle profiles remain in place for years

- Depreciation assumptions stop reflecting current vehicle markets

- Flat increases are added over time without refreshing cost data

- Vehicle retention cycles no longer match real-world ownership patterns

Over time, those assumptions can slowly drift away from actual vehicle costs.

For example, a reimbursement program may continue using older vehicle pricing assumptions even after the cost of purchasing and insuring vehicles changes substantially in the market.

Or a provider may maintain reimbursement outputs through broad adjustments rather than rebuilding the underlying vehicle assumptions themselves.

That does not automatically make a program non-compliant. But it can make the methodology harder to explain, maintain, and defend over time.

And so the real question companies should be asking is: does the reimbursement methodology still reflect what vehicles actually cost today?

That matters far more than comparing reimbursement numbers in isolation.

What Is a Fixed Cost Adjustment (FCA)?

This is where the conversation around FAVR reimbursements can become more technical. Sometimes providers apply something called a Fixed Cost Adjustment (FCA).

An FCA is an adjustment made to the fixed-cost portion of a FAVR reimbursement, which includes ownership-related expenses like:

- Insurance

- Depreciation

- Registration fees

- Taxes

- Licensing costs

Similarly, a Variable Cost Adjustment (VCA) is a strategy used to adjust the variable portion of FAVR reimbursement for expenses like tires and maintenance.

These flat cost adjustments can create compliance risk when they are used to maintain targeted reimbursement levels without updating underlying vehicle assumptions or supporting the adjustment with clear business rationale.

In practice, this can look like:

- Applying flat percentage increases or dollar adjustments to fixed costs

- Maintaining outdated vehicle profiles long after market conditions change

- Preserving reimbursement outputs without tying them back to current ownership costs, localized market data, or actual job-related driving requirements

Over time, unsupported adjustments can create real challenges. Companies may find it harder to explain how reimbursement rates were calculated, show that assumptions still reflect current market conditions, or maintain consistent and fair outcomes across employees, locations, and vehicle types.

Like most parts of FAVR, the real issue is not whether an FCA exists. The important question is whether the reimbursement methodology remains practical, transparent, and connected to real-world vehicle costs over time.

Examples of Compliant Program Adjustments

In many cases, changes to a FAVR program are both reasonable and necessary to keep mileage reimbursements aligned with real business-driving conditions.

The key is whether those adjustments stay tied to compliant program methodology, localized market data, and legitimate business-driving requirements.

Here are some examples of adjustments that may increase or reduce reimbursements over time:

For example, a company with employees covering large territories or transporting equipment might need a larger standard vehicle with higher ownership costs.

On the other hand, companies focused on cost control might choose to move toward more value-oriented vehicle assumptions or longer retention cycles.

Fixed and Variable Cost Adjustments (FCAs and VCAs) can still support compliance when they’re backed by clear documentation and a well-defined rationale.

For example, condition-based adjustments designed to support active drivers in regions with extreme weather may be considered defensible when they account for higher depreciation, increased tire wear, and additional maintenance costs.

Neither approach is inherently right or wrong. What matters is that reimbursement rates continue reflecting current costs and clearly defined business-driving requirements, rather than relying on assumptions that no longer match real-world conditions.

Cardata’s Methodology Explained

At Cardata, our methodology for creating audit-defensible rates is built around using compliant program assumptions, real-world cost data, and ongoing program management to calculate reimbursements that reflect the actual business-required cost of owning and operating a vehicle for work.

That methodology defining and adjusting includes:

- Company-defined vehicle standards (ex. vehicle class and MSRP, retention cycle, insurance requirements, Business Use Percentage (BUP))

- Localized cost data (fuel, insurance, depreciation, maintenance, registration, taxes, regional operating costs)

- IRS-compliant FAVR calculation rules (ex. separating fixed ownership costs from variable driving costs, clear documentation and rationale of any required adjustments relevant outside of typical program inputs)

- Ongoing program maintenance and optimization to keep rates aligned with current market conditions over time (ex. mileage bands)

Why IRS-Compliant FAVR Programs Need Ongoing Updates

The IRS framework behind FAVR exists for a reason. Vehicle costs are not static. Driving conditions vary by region. Vehicle ownership costs vary by market. Mileage patterns vary by employee role.

A reimbursement program built around real-world driving costs needs ongoing maintenance to stay accurate. That is why IRS-compliant FAVR programs rely on several foundational pieces, including:

- Mileage tracking

- Current cost data

- Standard vehicle profiles

- Ongoing reimbursement updates

- Geographic cost localization

These requirements are not there to create complexity for employers. They exist because business-driving costs naturally change over time.

Programs that update regularly are generally easier to explain, easier to maintain, and easier to support during audits or internal reviews.

According to Cardata’s Fleet Market Survey 2026, only 45% of organizations say they feel extremely confident in IRS compliance, while 37% say they lack trusted reimbursement data sources for maintaining fair and standardized rates.

This highlights a growing challenge for organizations managing reimbursement programs with outdated tools or inconsistent methodologies.

Why This Matters for Companies

For businesses, this conversation is about more than reimbursement math. It affects fairness, transparency, administration, and employee trust.

When reimbursement methodology stays clear and up to date, the whole program tends to run more smoothly. Employees have an easier time understanding how their reimbursement is calculated and why rates may shift over time.

Finance teams can budget and forecast with more confidence because the numbers stay tied to current vehicle costs instead of outdated assumptions.

HR teams are also better positioned to support fairness across different regions and driving roles, while the company as a whole has an easier time explaining and defending the program if questions ever come up.

In the long run, keeping the methodology current usually means fewer manual fixes, fewer employee questions, and less administrative headaches overall.

The Methodology Matters More Than the Number

The goal of a FAVR program is not to preserve reimbursement levels forever. The goal is to reimburse employees fairly for legitimate business-driving costs while keeping the program current, cost effective, supportable, and aligned with real-world conditions.

Vehicle markets evolve constantly.

Fuel prices change. Insurance changes. Depreciation changes. Vehicle ownership costs change.

Reimbursement methodology should evolve too.

That is why comparing two FAVR rates without understanding the assumptions behind them only tells part of the story.

The methodology behind the reimbursement matters just as much as the reimbursement number itself. At Cardata, we believe reimbursement programs should remain transparent, localized, data-driven, and easy to explain over time.

That means regularly updating vehicle assumptions, maintaining current market data, and ensuring reimbursement logic continues reflecting the real cost of business driving.

If your organization is reviewing its FAVR program or comparing reimbursement providers, the most important thing to evaluate is not just the rate itself, but how that rate is built and maintained over time.

If you want help evaluating your current program or understanding how your reimbursement methodology compares to today’s market conditions, Cardata’s team can help.

Talk to Cardata

.jpg)