.webp)

If your employees use their personal vehicles for work, you need a reimbursement program that’s accurate, fair, and tax-compliant. That’s where FAVR comes in.

FAVR stands for Fixed and Variable Rate. It’s a structured vehicle reimbursement program approved under IRS guidelines that allows employers to reimburse drivers tax-free. Instead of paying a flat allowance or a single cents-per-mile rate, FAVR separates the real costs of driving into two parts.

The fixed portion covers ownership costs like depreciation, insurance, registration, and taxes. These are the costs a driver carries simply by having a vehicle available for work. The variable portion reimburses operating costs like fuel, maintenance, and tires based on actual business miles driven.

Together, those two components create a reimbursement model that reflects what it truly costs to drive for business, without putting vehicles on your balance sheet.

Building a FAVR program takes structure, but it’s not guesswork. When you break it down step by step, the process becomes clear and manageable.

Here’s how it works.

Step 1: Choose Your Program Standard Vehicle

Every FAVR program starts with a standard vehicle profile. This is one of the most important building blocks in the FAVR structure.

The “standard vehicle profile”, otherwise known as the base vehicle model, represents the type of vehicle required for the employees’ roles. It does not tell employees what they have to drive, drivers still choose their own vehicles based on their preferences and needs.

The standard vehicle simply creates a consistent benchmark for calculating reimbursement. Think of it as the reference model the company uses to determine fair and compliant rates for the respective employee population.

Why does this matter?

Because vehicle costs are not the same across the board. Fuel economy varies. Insurance premiums differ by vehicle class and driving requirements.

Depreciation can change significantly depending on price and resale value. Maintenance costs are not identical between a compact sedan and a midsize SUV. Without a standard reference point, reimbursements can become inconsistent, inflated, or difficult to justify.

A standard vehicle profile brings structure to the program. It defines a reasonable vehicle class for the role, sets an appropriate MSRP range, and establishes a retention cycle. That keeps calculations predictable and defensible while still giving employees flexibility in their personal vehicle choice.

Step 2: Set the Business Use Percentage (BUP)

Next, you’ll determine the Business Use Percentage (BUP).

The BUP reflects how much of a vehicle’s total use is expected to be for business purposes. In IRS-compliant FAVR plans, a common starting point is 71.4 percent. That reflects five business days out of seven.

This percentage matters because it determines what portion of fixed vehicle costs can be reimbursed tax-free.

Setting the BUP correctly keeps the program aligned with IRS accountable plan rules, helps ensure reimbursements remain tax-free, and reduces the risk of overpayment or underpayment across drivers.

This isn’t guesswork. It’s a documented, structured input for the program.

Step 3: Factor in Driver Location

Not all driving costs are national averages.

Insurance premiums vary by state. Registration fees vary by province or county. Fuel prices vary by ZIP code. Even taxes and title fees change by region.

That’s why FAVR programs are location-sensitive.

Each driver’s home address and territory are factored into the reimbursement calculation. This ensures drivers in higher-cost areas are not underpaid, and drivers in lower-cost regions are not overpaid.

Location-based reimbursement is one of the main reasons FAVR programs are considered more accurate than flat car allowances or national average mileage rates.

Step 4: Assign Mileage Bands

A mileage band is just a projected range of how many business miles a driver is expected to put on their vehicle in a year. It sounds simple, but it plays an important role in keeping a FAVR program fair.

Mileage matters because it directly impacts depreciation, maintenance, and resale value.

A driver putting 30,000 business miles on their car each year will wear it down much faster than someone driving 10,000. More miles mean more maintenance, faster depreciation, and a lower resale value when it’s time to replace the vehicle.

Mileage bands allow the fixed portion of the reimbursement to reflect that difference. Drivers who are expected to drive more fall into higher mileage bands, which adjusts the fixed reimbursement to account for the added wear and tear over time.

It’s important to understand that mileage bands only affect fixed costs. Variable costs are still reimbursed per mile based on actual business mileage. If someone drives more in a given month, they’re reimbursed for those extra miles through the variable rate.

When handled properly, mileage bands keep things balanced. High-mileage drivers aren’t left subsidizing the program, and low-mileage drivers aren’t overpaid. And because the structure is built into the program from the start, it doesn’t create extra administrative work down the road.

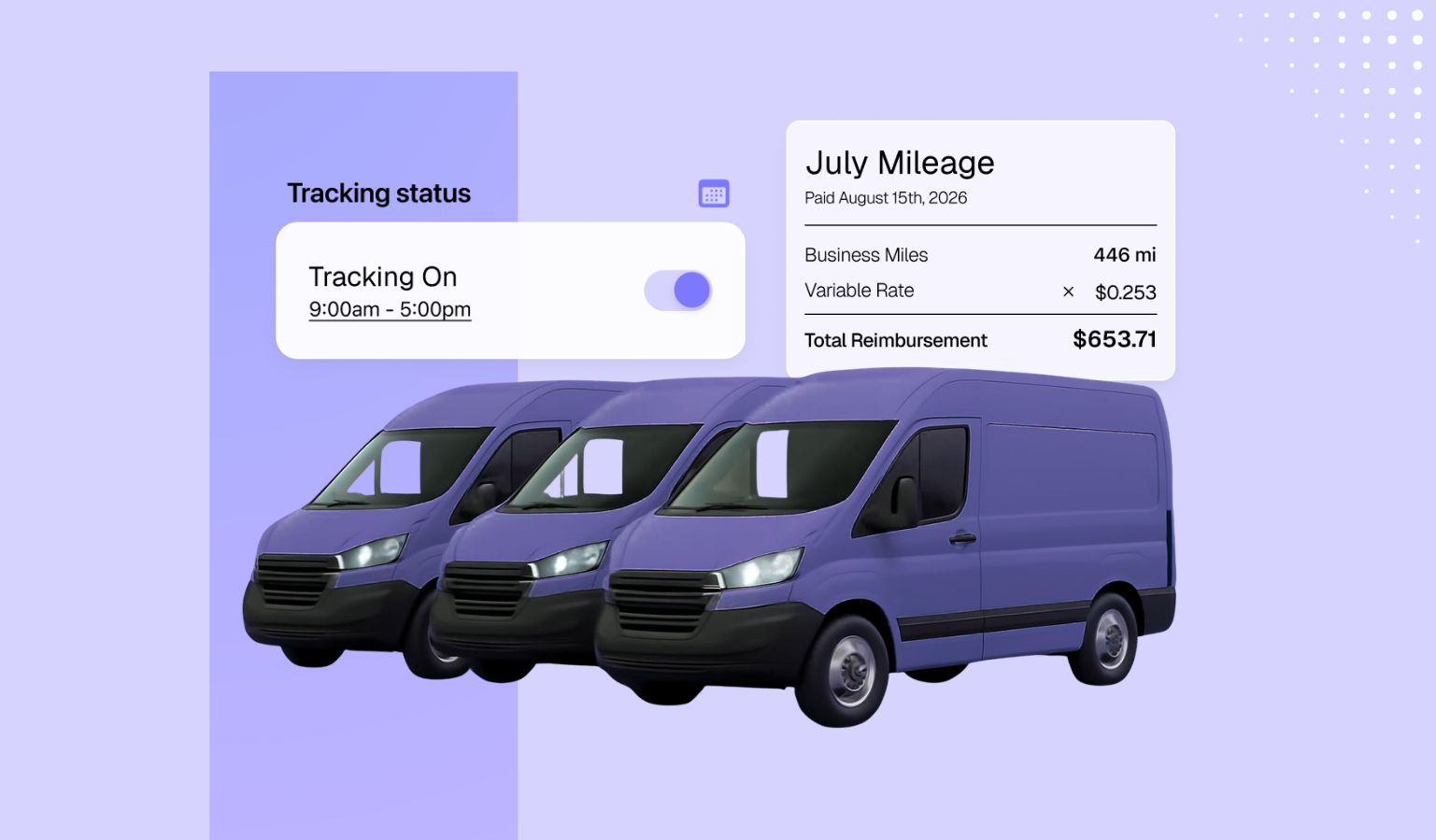

Step 5: Separate Fixed and Variable Costs

This is where FAVR gets its name. A FAVR reimbursement is built on two separate components that work together to reflect the true cost of driving for work.

The first piece is the fixed cost reimbursement. This portion is paid monthly and covers the basic costs of owning a vehicle. That includes depreciation, insurance, license and registration fees, and applicable taxes.

These are expenses a driver takes on simply by having a car available for business use. They exist whether the vehicle is driven that month or not. In simple terms, these are the costs required to put a car in the driveway and keep it there legally and insured.

The second piece is the variable cost reimbursement. This is paid per business mile driven and covers the costs that increase as mileage increases.

Fuel is the most obvious example, but it also includes routine maintenance, tires, oil changes, and general wear and tear. The more someone drives for work, the more these costs add up.

Because fuel prices, repair costs, and maintenance expenses change throughout the year, variable rates are updated regularly to stay aligned with current market data. That ongoing adjustment is important. It prevents overpaying when costs drop and underpaying when costs rise.

This two-part structure is what makes FAVR different from a flat car allowance or a simple Cents-Per-Mile rate. By separating ownership costs from operating costs, FAVR stays accurate, tax-compliant, and fair over time.

Step 6: Automate Tracking and Compliance

For a FAVR program to stay tax-free, it has to follow IRS accountable plan rules. That means business mileage must be properly documented, commute miles have to be excluded, drivers need to meet minimum annual mileage requirements, and vehicles must stay within age and value limits.

On paper, that all sounds manageable. In reality, once you’re dealing with multiple drivers across different territories, it can get complicated fast. Spreadsheets multiply. Odometer declarations get missed. Rates go stale. Small errors turn into bigger compliance risks over time.

That’s why most organizations rely on reimbursement software to handle the heavy lifting. Automated systems can track mileage as it happens, adjust rates based on location, verify insurance coverage, and maintain clean, audit-ready documentation without constant manual oversight.

According to Cardata’s Fleet Market Survey 2026, many organizations still rely on outdated manual processes, which increases both error risk and administrative workload. Automation changes that. It makes the experience easier for drivers and removes the compliance guesswork for finance and HR teams.

Why a FAVR Partner Matters

At this point, you might be thinking: this sounds like a lot to manage.

And you’re not wrong. A FAVR program requires current cost data, accurate mileage tracking, annual odometer declarations, eligibility monitoring, and vehicles that meet IRS age and value requirements. Policies need to be written clearly and applied consistently so reimbursements stay tax-free.

Handled manually, that can feel like a full-time job.

If those pieces aren’t actively maintained, risk builds over time. Rates can become outdated, and drivers can fall below eligibility thresholds. Documentation gaps can create audit exposure.

Even a well-designed program can drift if no one is keeping it aligned.

The good news is you don’t have to manage this on your own.

This is where the right partner makes a difference. A mileage reimbursement partner like Cardata handles the administrative side of the program, from calculating location-based fixed and variable rates, to tracking mileage, collecting odometer declarations, verifying insurance, and maintaining audit-ready documentation.

Instead of relying on spreadsheets and manual oversight, your HR and finance teams can stay focused on their core responsibilities. The compliance framework runs in the background, rates stay current, and the program scales as your team grows.

FAVR is built on structure. A strong partner helps you keep that structure intact without adding workload to your internal team.

The Bottom Line

Setting up a FAVR program is not about adding complexity. It is about replacing guesswork with structure.

When built correctly, a FAVR program aligns reimbursements with real driving costs, keeps payments tax-free under IRS rules, adjusts for geographic and mileage differences, reduces administrative burden, and improves fairness across drivers.

If you are transitioning from fleet vehicles or replacing a flat car allowance, the setup process is more manageable than it may seem. Once implemented, the program operates on clear rules, documented inputs, and consistent updates. That structure is what makes it sustainable over time.

Talk to a FAVR Expert

.jpg)