Navigating IRS mileage reimbursement rules can feel complicated, especially as businesses try to balance compliance, tax efficiency, and fair compensation for employees who drive their personal vehicles for work.

Whether you reimburse using the IRS standard mileage rate, a FAVR program, or a tax-free car allowance, the IRS has clear guidelines on what counts as business mileage, how rates are determined, and what documentation employers must maintain to keep reimbursements tax-free.

These rules matter because getting them wrong can create tax liability for employees, unexpected payroll costs for employers, and compliance risks during an audit.

And with mileage rates, driving costs, and state-specific reimbursement laws changing frequently, many organizations struggle to understand what’s required, or even which program structure they should be using.

This guide breaks down the 2026 IRS mileage reimbursement rules, explains how they apply across different program types, clarifies what counts as business mileage (and what doesn’t), and covers how federal and state laws interact.

What Are the IRS Mileage Reimbursement Rules?

The IRS mileage reimbursement rules outline how employers can reimburse employees for business-use driving on a tax-free basis.

To qualify, reimbursements must follow an “accountable plan.” An accountable plan is an IRS-approved employer plan used to reimburse employees for business-related expenses without the reimbursements being considered taxable income or wages.

It means employees must track and substantiate their business miles with compliant logs, and payments cannot exceed the IRS standard mileage rate unless using a program like FAVR.

In an accountable plan for vehicle reimbursement, excess funds generally need to be returned to maintain IRS compliance. The program tracks mileage against the IRS standard rate, and any excess reimbursement over that rate is taxable.

https://www.youtube.com/watch?v=t65jU2VeVuI

Core IRS Rules That Apply to All Mileage Reimbursement Programs

Before choosing a reimbursement model, it’s essential to understand the IRS rules that apply to every program. These rules determine whether reimbursements stay tax-free or become taxable income. Here are the core requirements all businesses must follow:

1. Business vs. Personal Mileage

The IRS only allows tax-free reimbursement for business-use mileage. This includes trips to client meetings, job sites, or any location that is not the employee’s primary workplace.

Commuting miles (travel between home and a regular work location) are always considered personal and cannot be reimbursed tax-free. Mixing personal and business miles can invalidate a program and create tax liability for both employer and employee.

Here’s some examples of types of trips, and whether they fall under “business” or “personal mileage.”

- Driving from the office to a client site = business mileage.

- Driving from home to the office = personal mileage.

- Driving from Client A to Client B = business mileage.

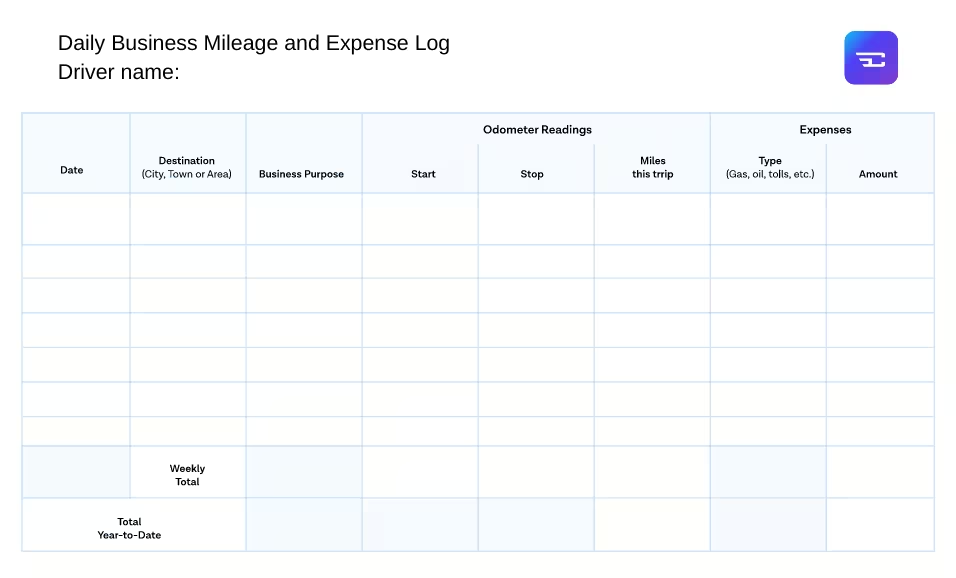

2. Documentation Requirements

Every tax-free reimbursement must be backed by accurate, audit-ready mileage logs, and the IRS generally requires that these records be kept for three years. Logs must include:

- Start and end odometer readings

- Total miles driven

- Business purpose of the trip

- Destination address

- Any related expenses (e.g., tolls)

Paper logs are technically allowed, but easy to misplace or miscalculate. Mileage tracking apps simplify compliance by capturing all required information automatically.

3. Accountable Plan Rules

To remain tax-free, reimbursements must follow the IRS’s accountable plan standards. This means:

- The expense must have a clear business purpose

- The employee must substantiate mileage with proper logs

- Employers must not overpay; any excess reimbursement becomes taxable

If these conditions aren’t met, the payment is treated as taxable income.

4. IRS Standard Mileage Rate Limits

For CPM and TFCA programs, reimbursements must stay at or below the IRS standard mileage rate to remain fully tax-free.

This rate changes at least once a year (typically in December or January) and occasionally midyear if driving costs spike. For example, in 2022 the IRS increased the rate midyear due to rising fuel prices.

Because the standard rate fluctuates with real-world costs like fuel, insurance, and depreciation, employers must monitor IRS updates to keep their programs compliant.

IRS Rules for Mileage Reimbursements Explained By Program

Not all mileage reimbursement programs follow the same IRS requirements. While the goal of each program is the same (fair, tax-free reimbursement for business driving) the IRS sets different rules depending on how the reimbursement is calculated.

The Cents Per Mile method (CPM) is the most straightforward, because it follows the IRS standard mileage rate.

Then, there’s the Fixed and Variable Rate (FAVR) program, and Tax Free Car Allowance (TFCA). These two programs are based on the driver’s actual costs of owning and operating a vehicle.

The following breakdown walks through the IRS rules for each of these reimbursement models, so you can choose and operate your vehicle reimbursement program confidently.

1. Rules for Cents Per Mile Programs

The Cents Per Mile (CPM) program is a very straightforward reimbursement method, because it follows the IRS standard mileage rate. Its core rule is simple: You reimburse employees a set amount for every business mile they drive, and as long as that rate is at or below the IRS limit, the payment stays tax-free.

For 2026, the IRS standard mileage rate is set at 72.5 cents per mile. If you reimburse employees at 72.5 cents or below, the entire amount is tax-free.

But if you pay above the IRS rate (for example, 75 cents per mile), the extra 5 cents is considered taxable income. That portion is subject to both payroll tax for the employer and income tax for the employee.

This simplicity is what makes CPM easy to administer compared to other program types.

2. Rules for FAVR Programs

Fixed and Variable Rate (FAVR) reimbursement rules are more complex than CPM because the IRS wants to ensure these programs reimburse true business expenses. They are watching out to make sure the program isn’t used to provide hidden income.

To stay compliant, it’s important to follow specific rules related to the drivers on the program, how much they drive, and what vehicles they use.

- Minimum number of drivers. A FAVR program must include at least five drivers. This means the program is intended for organizations of a certain size. Small businesses can still qualify, but only if they have at least five employees who drive for work.

- Minimum number of miles driven. Each driver must also log at least 5,000 business miles per year. If your drivers only travel 2,000 business miles annually, they do not qualify for FAVR and cannot be reimbursed using this methodology.

- Insurance. An employee's insurance coverage must be equal to or greater than the standard insurance required by the company.

- Minimum vehicle MSRPs. FAVR also sets rules for vehicle cost and age. When new, the MSRP of the car driven by the employee must be at least 90% of the standard vehicle cost chosen by the company (as included in their FAVR vehicle profile).

- Retention cycles. Every FAVR program must include a retention cycle, which is a company-defined vehicle age limit. Whatever cycle length you choose determines how old an employee’s vehicle can be to remain eligible for tax-free reimbursement.

Once all of these requirements are built into your policy, your FAVR program will meet IRS rules for tax-free reimbursement. As long as drivers remain compliant with the program requirements, their reimbursements will not be taxed, and employers will not owe payroll taxes on those payments.

3. Rules For Tax Free Car Allowance Programs

Tax-Free Car Allowance (TFCA) programs (often called “accountable car allowances”) work much like traditional car allowances but with one key difference: All business expenses must be properly accounted for.

The IRS has two main requirements for TFCA programs: Employers must track business mileage, and they must compare each driver’s reimbursement to the IRS standard mileage rate.

A TFCA can be structured in several ways. You can use a single variable rate (ex. 62.5¢ per mile), a flat monthly allowance (such as $700), or even a FAVR-style setup with separate fixed and variable payments.

Any structure is acceptable as long as, at the end of the day, the total reimbursement is tested against the IRS standard rate. If a driver effectively receives $0.70 per mile when the IRS rate is 62.5¢, the excess is taxable and must be treated as income.

Detailed rules and examples for calculating TFCA reimbursements are outlined in IRS Publication 463.

State Mileage Reimbursement Rules: Key US States Explained

When it comes to mileage reimbursement, each state in the US has its own set of rules and regulations that govern how employers should compensate their employees for business-related travel.

While most states adhere to federal guidelines for mileage reimbursement, there are exceptions. Read on to learn the specific mileage reimbursement rules in key states.

States That Follow Federal Rules

The US states Ohio, Georgia, Michigan, Florida, New York, Pennsylvania, and North Carolina generally defer to the federal IRS mileage reimbursement guidelines.

This means that these states do not impose additional reimbursement requirements on private employers. Businesses typically follow the IRS standard mileage rate when compensating employees for business-related driving.

While state agencies or workers’ compensation programs may have their own mileage rules, private-sector employers in these states are not obligated to go beyond federal standards, making compliance more straightforward than in states with their own reimbursement mandates.

States With Strict Reimbursement Rules

Massachusetts, California, and Illinois have unique regulations.

1. Massachusetts Mileage Reimbursement Rules

In Massachusetts, the mileage reimbursement rules stand out from the federal norms. Employers in the state are required to reimburse employees for the “reasonable expenses” incurred during business-related travel. This means that employers must cover all reasonable and necessary expenses related to the use of a personal vehicle for work purposes, including mileage.

2. California Mileage Reimbursement Rules

Similar to Massachusetts, California has specific mileage reimbursement rules that exceed federal guidelines. Employers in California are legally obligated to reimburse employees for all necessary expenditures they incur while performing job-related tasks. This includes mileage as well as other costs associated with vehicle usage.

3. Illinois Mileage Reimbursement Rules

Illinois also deviates from the federal standard by requiring employers to reimburse employees for necessary job-related expenses, which includes mileage. The key difference in Illinois is that employers are obligated to cover these expenses even if they don’t have a written reimbursement policy in place.

States With Unique State-Employee Rules

4. Minnesota Mileage Reimbursement

For both state employees and private employers, Minnesota has clearly defined guidelines that diverge slightly from federal IRS standards. State employees qualify for different rates depending on whether a state-owned vehicle is available, while private employers are encouraged (but not legally required) to follow the IRS rate.

5. Maine Mileage Reimbursement

Maine relies on a framework that aligns partially with federal guidelines, but it also sets its own rates for state employees, typically 75% of the federal rate. For private employers, adopting the IRS rate is common, though not mandated.

6. Mississippi Mileage Reimbursement

While Mississippi generally follows the IRS rate for mileage reimbursement, the state has specific rules for its employees (including reduced rates if a state vehicle is offered) and mandatory coverage for Workers’ Compensation travel.

7. Kentucky Mileage Reimbursement

In Kentucky, private employers are free to choose a policy, often matching the IRS rate, while state employees receive reimbursements tied directly to average fuel costs. Regular quarterly adjustments ensure rates for state workers reflect real-time price changes.

8. Louisiana Mileage Reimbursement

Louisiana mandates a 72.5 cents-per-mile rate for 2026 for state employees, with additional rules for Workers’ Compensation–related travel. For private employers, there’s no legal requirement to reimburse mileage, unless connected to Workers’ Comp.

9. Kansas Mileage Reimbursement

State employees in Kansas have different per-mile rates depending on the type of vehicle (cars, motorcycles, or airplanes) and private employers typically align with the IRS standard. Detailed mileage logs and thorough documentation keep both employers and employees compliant and fairly compensated.

10. Iowa Mileage Reimbursement

State employees in Iowa must follow Iowa Code §8A.363, which ties reimbursements to the IRS rate. Private employers often match that rate but may set their own standards.

11. Idaho Mileage Reimbursement

Idaho typically follows IRS guidelines, but state employees must abide by Section 67-2004 for official travel reimbursements. Workers’ Compensation mileage is mandatory for job-related medical appointments, and private employers can create custom programs like FAVR or Tax-Free Car Allowance.

12. Hawaii Mileage Reimbursement

In Hawaii, state employees have a clear right to mileage reimbursement under Code §3-10-13, usually aligned with the IRS rate. Private employers aren’t required to reimburse, except in certain Workers’ Comp scenarios. Keeping records and clarifying policies are essential.

13. Delaware Mileage Reimbursement

Delaware’s state employees receive a set rate (50¢ per mile), but private employers usually follow either Delaware’s state rate or the IRS rate. Important topics include preventing wages from slipping below minimum wage, plus special rules for Workers’ Compensation travel.

14. Connecticut Mileage Reimbursement

There’s no strict reimbursement law for private companies in Connecticut, so employers often use the IRS rate. However, workplace injury travel is reimbursable under Workers’ Compensation, and minimum wage laws may require additional payments for heavy drivers.

15. Alabama Mileage Reimbursement

Alabama requires that state employees be reimbursed at the IRS rate (72.5 cents in 2026), and private employers have no statutory mileage obligation—except for Workers’ Comp–related travel. Many businesses opt to follow the federal standard or set up a formal reimbursement program.

16. Alaska Mileage Reimbursement

For state employees, Alaska law references the IRS rate for official travel, while Workers’ Compensation mandates mileage coverage for medical appointments. Private employers don’t have a legal reimbursement requirement but frequently adopt the IRS rate to reduce wage compliance issues.

17. Arkansas Mileage Reimbursement

In Arkansas, state employees must be reimbursed at the published rate (72.5 cents per mile in 2026), and Workers’ Comp mileage is obligatory. For everyday business travel, private employers aren’t bound by law but often mirror federal standards. Tech tools and recordkeeping tips can smooth out the process.

18. Colorado Mileage Reimbursement

Colorado applies unique reimbursements of 90% of the IRS rate for 2WD and 95% for 4WD vehicles for state employees. Private employers typically use or approximate the IRS rate. Staying above the minimum wage and preserving accurate logs are key considerations.

19. Wisconsin Mileage Reimbursement

Wisconsin generally follows the IRS guidelines, although state employees may see variations approved by the Division of Personnel Management (DPM). Employers and employees alike need to keep close track of mileage logs to avoid wage or tax issues.

20. Missouri Mileage Reimbursement

No law forces private employers in Missouri to follow the IRS rate, yet most do to keep calculations simple. State employees, however, abide by set policies, and Workers’ Compensation mileage is required. Here’s how to stay compliant and plan effectively.

21. Maryland Mileage Reimbursement

Maryland doesn’t impose strict rules on private employers, but many match the IRS rate to maintain fairness and avoid wage pitfalls. For state employees, guidelines often align with federal norms. Carefully logging mileage and understanding the FLSA are critical.

22. Indiana Mileage Reimbursement

Indiana does not mandate a specific rate for private employers; the IRS standard remains the practical choice for most. Drivers should keep detailed logs to deduct travel costs at tax time, and minimum wage compliance can come into play with extensive driving.

23. Tennessee Mileage Reimbursement

Like other states, Tennessee lacks a formal private-sector mandate, but state agencies typically follow or approximate the IRS rate. If employee expenses drive their effective wage below the minimum, employers must compensate.

24. Washington Mileage Reimbursement

Washington State also abides by the federal IRS rate in most private contexts. That said, private businesses should ensure reimbursement programs don’t push wages under the federal minimum. Digital mileage tracking and consistent policies help both parties.

25. Arizona Mileage Reimbursement

Arizona defers to federal guidelines, so private employers often adopt the IRS standard. As with most states, employees’ effective pay can’t sink below minimum wage due to travel costs, and thorough mileage tracking is crucial for all.

26. Virginia Mileage Reimbursement

Virginia doesn’t require private employers to reimburse mileage, but many choose to do so at or near the IRS rate. Key points include ensuring employees aren’t shorted below minimum wage and that mileage logs meet IRS criteria.

How to Stay Aligned With IRS and State Mileage Rules

Mileage reimbursement rules in the United States can vary significantly from state to state. While most states adhere to federal guidelines for mileage reimbursement, Massachusetts, California, and Illinois have distinct regulations that require employers to provide more comprehensive compensation for business-related travel.

It’s important to be well-informed about these rules to ensure compliance and fair compensation. Whether your state follows federal guidelines or has specific regulations, understanding the intricacies of mileage reimbursement is crucial for a smooth and transparent employer-employee relationship.

The IRS rules can be complex, but your reimbursement program doesn’t have to be. Cardata helps businesses design and operate tax-free, fully compliant vehicle programs, whether you use CPM, FAVR, or a tax-free car allowance.

From automated mileage tracking to accurate rate calculations and seamless driver payments, we handle the details so your team can focus on their work.

Want to see how much you could save, and how much risk you can eliminate? Talk to a Cardata reimbursement expert today and get a tailored assessment for your business.

Book a demo with Cardata

.webp)

.jpg)