Choosing how to reimburse employees who use their personal vehicles for work isn’t always simple. Some teams default to a car allowance because it feels straightforward. Others pay per mile because it seems fairer.

But the truth is, the method you choose impacts taxes, compliance, take-home pay, administrative workload, and even employee satisfaction.

This guide breaks down the real differences between car allowances vs. mileage reimbursement, showing how each option works, where the tax pitfalls are, and which types of businesses benefit most from each approach.

By the end, you’ll know how to make a smarter, tax-savvy decision that protects both your budget and your employees.

Car Allowance vs. Mileage Reimbursement: What’s the Difference?

When businesses pay employees for using their personal vehicles for work, they usually choose between two methods: a car allowance or a mileage reimbursement. While both aim to cover driving expenses, they work very differently.

What is a Car Allowance?

A car allowance is a flat payment (usually given monthly, quarterly, or annually), which is added on top of an employee’s regular salary.

It’s simple: you pick an amount and pay it consistently to anyone who qualifies. Many companies list it as part of the job’s benefits package, and in most cases, every eligible employee receives the same amount, regardless of how much they actually drive.

The average car allowance has increased over time, but slowly. This is because many companies set their car allowance and forget about it, only updating the car allowance every few years.

What is Mileage Reimbursement?

A mileage reimbursement ties reimbursement directly to how many business miles an employee drives.

Someone in sales or distribution may rack up thousands of business miles a year, while an IT specialist might drive only occasionally. Mileage reimbursement ensures employees are compensated based on actual driving, not a one-size-fits-all stipend.

Tax Impact: Where Car Allowances and Mileage Reimbursements Diverge

The most critical difference between car allowances and mileage reimbursements is how the IRS treats each one. And for many employers, this is where costs can quickly spin out of control if you're not careful.

Car Allowances Are Usually Taxable

A standard car allowance is usually paid as a flat lump sum, and is almost always considered taxable income. Unless you take special steps to structure it under an IRS-approved accountable plan, that allowance will be taxed just like regular wages.

That means the allowance is added to the employee’s W-2 income, and they pay income tax on it. It also means that you, the employer, pay payroll taxes on it. If you don’t withhold the right amount, you could face a clawback or IRS audit.

It sounds simple, but the compliance risk and tax waste is real. For example, when an employer provides a $600 monthly car allowance, the cost includes significant tax waste due to IRS rules.

- On a $600 allowance, approximately $180 is lost to driver income tax.

- The employer pays about $46 in FICA tax.

- Total tax waste is roughly $226.

This means that an employee receiving a $600 car allowance, will take home only $420. For 100 employees, this can mean $271,200 lost annually.

Mileage Reimbursements are Tax-Free

Mileage reimbursement works differently. When done correctly, it’s one of the few ways businesses can provide truly tax-free payments to employees, because the IRS recognizes mileage reimbursement as a legitimate business expense, not income.

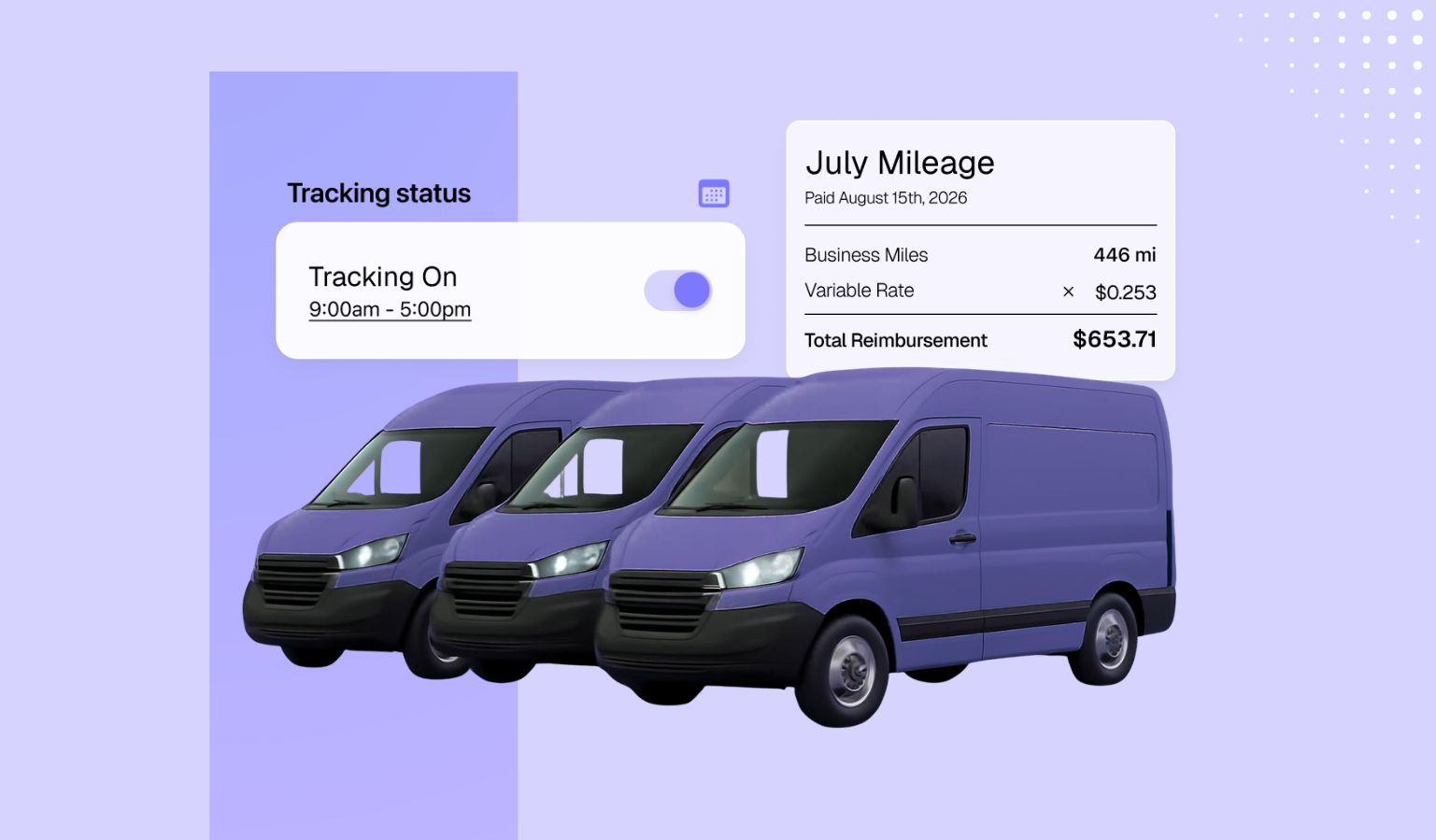

There are three mileage reimbursement programs to choose from: Fixed and Variable Rate (FAVR), Cents per Mile (CPM), and a Tax Free Car Allowance (TFCA). Most states use the federal standard mileage rate (set annually by the IRS) to determine the maximum tax-free amount.

For example, the standard rate in 2026 is 76 cents per mile.

Mileage reimbursement programs ensure employees are only paid for the miles they drive, and none of that payment is taxed when compliant.

Why Choosing the Right Method Matters

Picking between a car allowance vs. mileage reimbursement program isn’t just about preference. It has real financial and compliance consequences for your business.

The IRS has strict rules about what qualifies as a legitimate business expense, and if your program isn’t structured correctly, both you and your employees could face unwanted tax bills or audit exposure.

Car allowances are the biggest culprit here. Because they’re treated as taxable income, failing to withhold and report the proper taxes can trigger clawbacks, penalties, or even audits. A simple administrative choice can quickly become a compliance problem.

Mileage reimbursement programs, on the other hand, are designed to align with IRS requirements. When employees track mileage properly and your program follows IRS guidelines, these payments are considered non-taxable, helping you avoid compliance headaches while ensuring employees are reimbursed fairly.

Beyond taxes, the method you choose also affects budgeting predictability, employee satisfaction, and equity across your workforce. A poorly structured program can lead to overpaying some employees, underpaying others, or introducing fairness issues that impact morale.

Making an informed choice protects your business financially, keeps you compliant, and ensures employees feel supported and treated fairly.

Car Allowances: Pros and Cons

A car allowance is one of the simplest ways to pay employees who use their personal vehicles for work. But that simplicity comes with trade-offs. Here’s a clearer look at the real advantages and drawbacks.

Pros of Car Allowances

1. Simple to administer

A fixed monthly or annual payment is easy for HR and payroll teams to manage. There’s no mileage tracking, no variable payments. Just a predictable stipend added to an employee’s paycheck.

2. Appears fair on the surface

Since many businesses give every eligible employee the same allowance amount, it can feel equitable. Everyone gets the same benefit, which can simplify conversations around compensation.

3. Easy for employees to budget

With a set lump-sum payment which usually comes at the same time every year or month, employees know exactly what to expect. This consistency can help workers plan their expenses.

Cons of Car Allowances

1. You lose an over 30% to tax waste

Because car allowances are considered taxable income, employees lose a significant portion of the payment to taxes. This tax waste is entirely avoidable.

2. Payments aren’t actually equitable

If every employee gets $600 per month, but one drives in California and another in Texas, their real costs vary dramatically. Equal doesn’t always mean fair.

3. Employees may get pushed into a higher tax bracket

Adding an allowance to an employee’s salary can increase their taxable income, and potentially bump them into a higher bracket. They end up paying even more tax, without receiving more value.

Mileage Reimbursement: Pros and Cons

Mileage reimbursement offers a more precise, IRS-compliant way to compensate employees for business driving. It takes a little more administration than a flat allowance, but the benefits often outweigh the effort.

Pros of Mileage Reimbursement

1. Completely tax-free

This is the biggest advantage. Whether you use a simple Cents Per Mile (CPM) model or a structured program like Fixed and Variable Rate reimbursement (FAVR), compliant mileage reimbursements are not taxed. Employees keep more of their money, and employers avoid unnecessary payroll tax.

2. Cost-effective and accurate

Mileage reimbursement ensures you’re paying employees only for the miles they drive. This prevents overpayment while still fairly compensating high-mileage drivers.

3. More equitable for employees

Unlike a flat allowance, mileage reimbursement adjusts based on real driving needs. High-mileage employees aren’t underpaid, and low-mileage employees aren’t overpaid. This sense of fairness goes a long way. Employees feel valued, morale improves, and loyalty grows when pay aligns with actual workload.

Cons of Mileage Reimbursement

1. Potentially more administrative work

To stay compliant and tax-free, the IRS requires accurate documentation. That means your organization needs to collect mileage logs, and do regular reporting with detailed, accurate and timely records.

The good news? You don’t need to rely on manual logs, spreadsheets, or manual reporting. Modern mileage reimbursement platforms (like Cardata) take most of that burden off your plate.

These tools automatically capture mileage through a mobile app, eliminating handwritten logs and guesswork. They classify trips quickly, keep records clean and audit-ready, and generate the detailed, accurate, and timely reports the IRS requires.

Because compliance rules are built directly into the mileage reimbursement platform, both employers and employees stay aligned with IRS standards without needing extra oversight.

In short, mileage reimbursement platforms turn a time-consuming, error-prone process into a streamlined, automated workflow that keeps your program compliant and frees your team to focus on real work.

Mileage reimbursement is more work than a car allowance, but it’s also more accurate, more equitable, and more financially responsible for the business.

What to Consider When Choosing Car Allowance vs. Mileage Reimbursement

Although mileage reimbursement is usually the more efficient and compliant option, there are still a few important factors to weigh when deciding what’s right for your organization. Each business has different driving patterns, administrative resources, and policy constraints, so the best choice depends on how your team actually operates.

1. Driving Habits and Work Requirements

The IRS only considers business use of personal vehicles to be tax-deductible. That means it’s important to structure your program around the real needs of each role. Some employees (like sales reps and service technicians) rack up significant mileage. Others may only drive occasionally.

For low-mileage employees, a simple Cents Per Mile (CPM) program might be enough. For high-mileage drivers, a FAVR program may be more accurate and fair.

2. Tax Implications and Potential Savings

If you offer a lump-sum car allowance, employees need to understand that the payment is treated as taxable income. You’ll need to deduct the right amount of tax each pay period to avoid surprises at year-end.

A compliant mileage reimbursement program, on the other hand, can save your business significant money by eliminating tax waste, though you’ll need the right processes or tools to handle the added documentation requirements.

3. Policy Requirements

Even if you oversee the vehicle program, you may be limited by company policy. Leadership may prefer a certain approach or have legacy programs in place. Understanding policy constraints early on can save time and prevent frustration.

4. Record Keeping

The IRS requires mileage logs to be “detailed, accurate, and timely.” In practice, that means records should be collected at least every 30 days. If you’re considering a mileage reimbursement program, make sure your organization has the capacity (or technology) to manage consistent, compliant reporting.

Real-Life Scenarios: Choosing the Right Program for Your Team

Sometimes the best way to understand whether a car allowance or mileage reimbursement program makes sense is to see how each option plays out in real situations. Below are three common scenarios that show how different types of businesses might make the right choice.

Scenario A: A Startup With Several High-Mileage Drivers

You manage a growing startup with a sales team of 10 employees who all drive regularly. Each of them logs more than 5,000 business miles per year meeting with prospects, visiting client sites, attending trade shows, and supporting accounts in the field. With that much driving across the team, accuracy and fairness are critical.

Best setup:

A FAVR program is the strongest fit here. It provides a consistent fixed monthly payment for everyone on the team, while also adjusting the variable portion based on each driver’s actual mileage and local cost of driving.

This makes reimbursements far more accurate and equitable than a flat allowance, while keeping payments completely tax-free and compliant.

Scenario B: A Large Team With No Business Driving Needs

You oversee a team of 40 employees working at a call center. There’s no public transit nearby, so everyone drives to work. But aside from commuting, no one uses a personal vehicle for business purposes.

Best setup:

Since commuting is never tax-exempt under IRS rules, no mileage reimbursement program applies. In this case, offering a taxable vehicle allowance to offset commuting expenses could help with retention, especially in a high-turnover environment. It won’t save the business money, but employees will appreciate the support.

Scenario C: A Nonprofit With Infrequent Driving Needs

You’re the HR director at a nonprofit community services organization. Most employees don’t drive for work, but one outreach coordinator occasionally uses their personal vehicle for tasks like delivering donations, picking up supplies, or attending off-site community events.

These trips are irregular. Some weeks involve no driving at all, while other weeks include several short, unpredictable errands.

Best setup:

A Cents Per Mile (CPM) reimbursement is the simplest and most cost-effective choice. Since driving needs are infrequent and vary week to week, CPM ensures the employee is reimbursed fairly only when they actually drive for business, without the administrative overhead or complexity of a more structured program.

Creating a Fair, Compliant, and Cost-Effective Program

Deciding between a car allowance and a mileage reimbursement program isn’t just an administrative choice. It impacts taxes, fairness, employee satisfaction, and your overall compliance risk.

Car allowances may feel simple, but they create avoidable tax waste, can be inequitable, and often cost businesses far more than they realize. Mileage reimbursement programs, whether CPM, FAVR, or TFCA, offer a tax-free, compliant, and more accurate way to pay employees based on real business driving.

By understanding how each method works, and how factors like driving patterns, IRS rules, and record-keeping requirements come into play, you can make a more informed, cost-efficient decision for your organization.

With the right setup and tools, mileage reimbursement not only saves money but also improves transparency, fairness, and long-term employee trust.

If you're looking to optimize your program, reduce tax waste, or transition away from taxable allowances, a modern mileage reimbursement platform can help streamline compliance, automate documentation, and simplify the entire process for both your team and your drivers.

Want to learn how to build a more compliant, cost-effective vehicle program? Explore how a mileage reimbursement platform can help your organization lower risk, improve accuracy, and support your mobile workforce.

Talk to Cardata

.jpg)