What Are the Main Differences Between FAVR and TFCA Vehicle Reimbursement Models?

Introduction: Two IRS-Compliant Paths for Vehicle Reimbursement

For businesses deciding on the appropriate vehicle reimbursement method, specifically one that contains a fixed auto allowance, they often weigh the two IRS-compliant options: Fixed and Variable Rate (FAVR) and Tax-Free Car Allowance (TFCA). While both models aim to offer efficient and tax-advantaged personal vehicle reimbursements, they differ in structure, compliance requirements, and suitability for different operational needs and employee driving behaviours.

FAVR: Precision Based on Actual Costs

FAVR programs are structured to reflect the true business required cost of vehicle ownership and ongoing operation. FAVR reimburses employees based on estimated fixed costs such as depreciation, insurance, and license fees, as well as variable costs like fuel, maintenance, and tire wear. The model tailors reimbursements to location-specific costs for each employee so that payments are truly equitable. For example, an employee driving in a high-cost city would receive more than one located in a rural area, reflecting differences in fuel prices (https://cardata.co/blog/the-employers-guide-to-favr-car-allowances/).

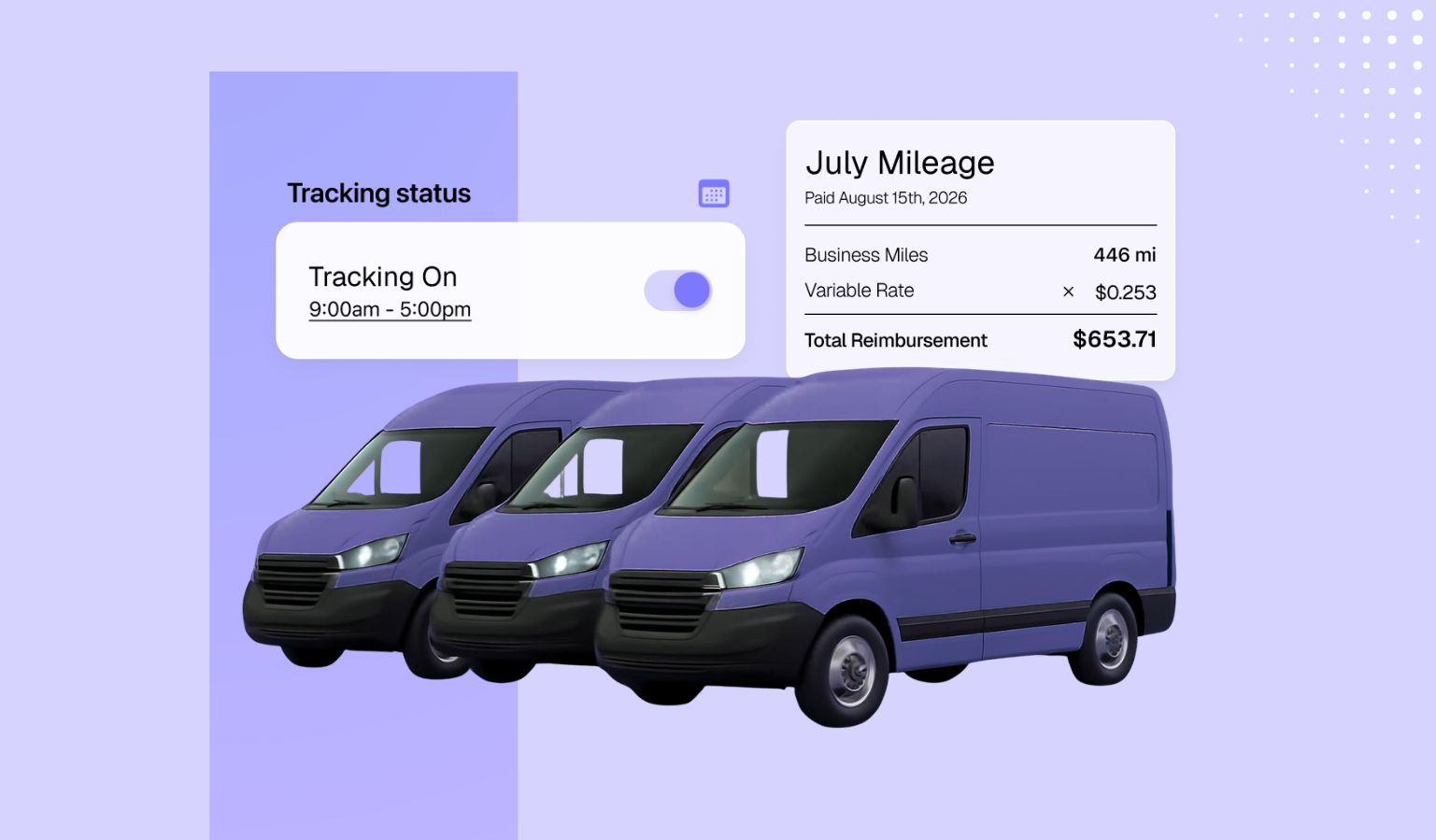

TFCA: Simplicity and Flexibility

In contrast, TFCA, also known as an “Accountable Allowance" utilizing IRS Publication 463, simplifies reimbursement and taxability calculations. Typically, companies establish a flat monthly allowance or a flexible rate based on estimated mileage, then they simply compare that allowance to the IRS standard mileage rate equivalent ($0.70 per mile in 2025). If the provided allowance exceeds this calculated threshold based on the employees’ actual reported mileage, only the surplus becomes taxable. If the difference is below the threshold, the payments are entirely tax-free (https://cardata.co/blog/understanding-irs-tax-rules-for-car-allowance-favr-accountable-and-taxable-allowance/).

Compliance Requirements: Rigid vs. Minimal

A key differentiator is compliance. FAVR programs have specific requirements: at least five employees must participate, each driving over 5,000 business miles annually. Vehicles used must fall within 90% of the base vehicle profile cost, and maintain insurance in line with company standards (https://cardata.co/blog/the-employers-guide-to-favr-car-allowances/). This makes FAVR ideal for larger workforces with consistent mileage patterns. In contrast, TFCA has minimal compliance requirements. Employers only need to track business mileage accurately and apply the "Tax Test," which ensures allowances don’t exceed tax-free thresholds (https://cardata.co/blog/understanding-tax-implications-of-vehicle-allowances-and-reimbursement-programs/).

Cost Efficiency and Savings Potential

FAVR offers superior precision in reimbursements and tax savings potential. Since it adjusts payments to actual market rates and employee driving profiles, it avoids under- or over-paying drivers. This often translates to significant cost savings—up to 30% compared to traditional taxable allowance models (https://cardata.co/blog/fixed-and-variable-rate-favr-reimbursement-programs/). It’s also worth mentioning that FAVR enables businesses to pay above the IRS standard rate equivalent: it’s the only tax-free method that allows this.

Budget Control and Administrative Ease

TFCA, however, provides greater rate creation flexibility and simplicity. Businesses can essentially choose to reimburse at any rate, and simply measure for tax. Because of this, TFCA is suited to companies seeking to control budgets or avoid compliance hurdles associated with more robust programs like FAVR. For example, TFCA can be applied uniformly across departments, locking in predictable costs month over month. It also works well when mileage varies widely among drivers, or employees drive less than 5,000 business miles per year (https://cardata.co/blog/understanding-irs-tax-rules-for-car-allowance-favr-accountable-and-taxable-allowance/).

Tax Treatment: FAVR Maximizes Tax-Free Potential

Another important distinction is taxation. FAVR reimbursements are entirely tax-free if IRS guidelines are followed. There are no payroll or income taxes deducted from payments if employees are compliant, maximizing the value received by employees and reducing the employer's tax burden (https://cardata.co/blog/what-is-a-favr-car-allowance/). In TFCA, reimbursements are only tax-free to the extent that they don’t exceed the IRS standard equivalent. Excess payments are treated as taxable income on the employee’s W2, making accurate mileage logging essential to avoid unintended taxes (https://cardata.co/blog/understanding-tax-implications-of-vehicle-allowances-and-reimbursement-programs/).

Adaptability and Strategic Use

TFCA also stands out for its adaptability. Employers can build rates using real market data, estimated mileage bands, or simply competitive intel, giving them strategic control over spend. This can be beneficial in industries with seasonal workloads, where vehicle usage fluctuates. Meanwhile, FAVR is best when consistency and cost optimization are top priorities, especially in high-mileage roles in sales or field service.

Administrative Complexity vs. Simplicity

FAVR programs require ongoing updates of vehicle costs, fuel prices, insurance, and maintenance trends. However, modern software platforms like Cardata streamline and automate these tasks, reducing the compliance burden while preserving the program's precision and tax advantages (https://cardata.co/blog/how-cardata-supports-fleet-managers/). TFCA, requiring only mileage logs and an annual tax test, is easier to administer but less granular.

Choosing the Right Model for Your Organization

Ultimately, choosing between FAVR and TFCA depends on your business goals. If the priority is to achieve the most accurate, tax-efficient reimbursement for a high-mileage workforce, FAVR is the best-fitting model. If administrative ease and consistent budgeting matter more, TFCA offers a viable, tax-advantaged alternative. Both approaches provide savings when compared to taxable car allowances and company-managed fleets, allowing companies to support mobile employees effectively while controlling costs.

Mixed Models for Workforce Diversity

Companies may also consider mixed approaches, using FAVR for core driving-focused roles and TFCA or CPM (Cents Per Mile) for occasional drivers. This ensures fairness, maximizes cost efficiency, and minimizes tax waste (https://cardata.co/blog/taxation-vehicle-reimbursement-favr-cpm-allowance/).

Assess, Customize, and Optimize

Each program, when properly implemented, will enhance employee satisfaction and financial clarity throughout an organization. When choosing the program of best fit, businesses should assess mileage patterns and corporate goals. Leveraging expert partners and data-driven tools, like Cardata, ensures compliance and long-term savings. Still unsure? Reach out to Cardata today, and we’ll help you select the program, or programs, of best fit.

Disclaimer: Nothing in this blog post is legal, accounting, or insurance advice. Consult your lawyer, accountant, or insurance agent, and do not rely on the information contained herein for any business or personal financial or legal decision-making. While we strive to be as reliable as possible, we are neither lawyers nor accountants nor agents. For several citations of IRS publications on which we base our blog content ideas, please always consult this article: https://www.cardata.co/blog/irs-rules-for-mileage-reimbursements. For Cardata’s terms of service, go here: https://www.cardata.co/terms.

.jpg)